Jul 16, 2013

Location Optimization: What Does it Mean?

A debate has surfaced in our industry over the last few years on what’s being called “location optimization.” Location optimization, or as some call it, “asset location,” is the practice of buying and holding investments based on the tax consequence the asset generates by holding it. For example, an average household’s portfolio may consist of a Traditional IRA, Roth IRA, and a taxable account (joint, trust, etc.). Each of these account types produces far different tax implications. Additionally, each investment in a diversified portfolio produces different tax consequences on a year-to-year basis.

Based on their objectives, a bond mutual fund will produce monthly or quarterly taxable dividends and interest. An emerging markets growth stock mutual fund will rarely produce a taxable dividend.

Location optimization would lead an investor to hold the bond mutual fund in an IRA, because the monthly dividend and interest payment would be completely tax deferred. If the investor held the fund in a joint or trust account, they would need to foot the tax bill at the end of each year. This lessens the “after-tax” investment return by up to a third.

Location optimization would lead an investor to hold the emerging markets stock fund in a Roth IRA (joint account if a Roth IRA is not available). Emerging market stocks tend to grow at a much higher rate (in the long run) than a bond. Thus, all the growth is completely tax-free (after age 59 ½) due to the tax treatment of the Roth IRA.

This is one example of where our firm stands on this debate. While we manage investment portfolios with this optimization in mind, it does have the potential to create widely varying investment returns on a “per account” basis. If we hold most of the fixed income (tax inefficient) investments in a Traditional IRA, and most of the growth stocks (tax efficient) in a Roth IRA or taxable account, the annual returns should be significantly higher in the accounts that hold a greater percentage of stocks. This may seem like common sense, but it can definitely lead to anomalies in investment performance if reviewing each account rather than the overall portfolio.

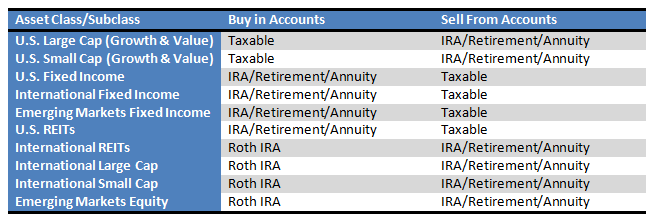

The chart below shows our preferred methods of holding each asset class in a diversified portfolio.